{kind=link}

{kind=link}

Some of the implications

for an existing Charitable Trust, as BSS used to be,

that have now registered as a CIO.

Information for BSS Members

Ahead of any formal Membership Approval, BSS

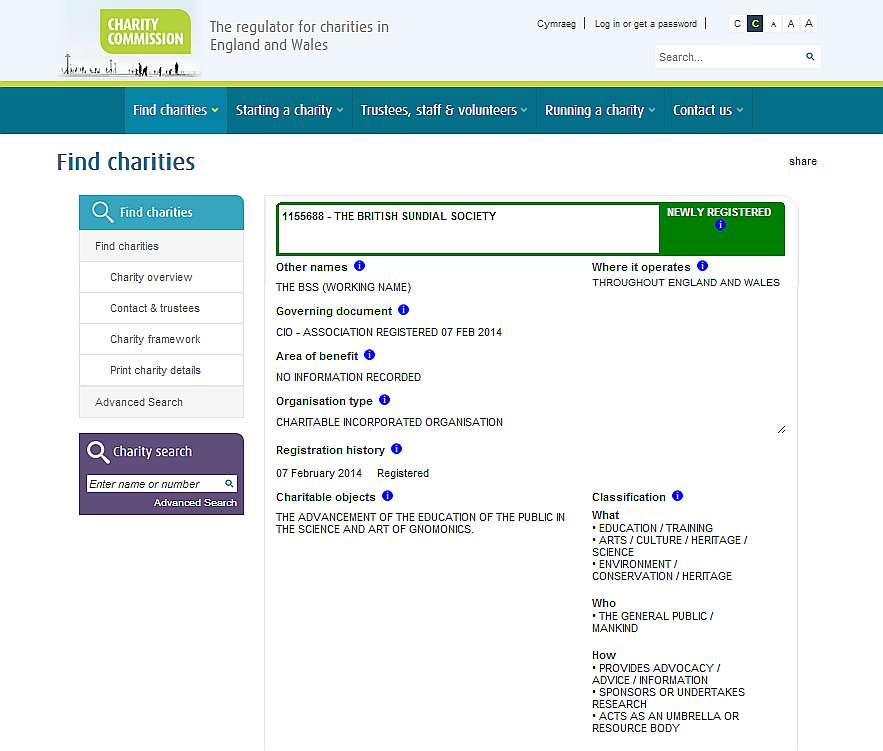

Trustees Registered a CIO on 7th February

2014: It is Charity 1155688

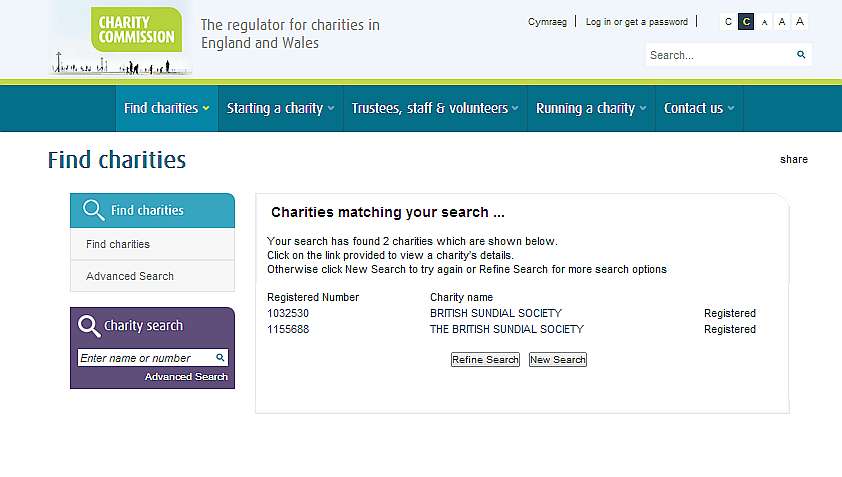

|►New

BSS CIO |►BSS

Charities|

Question: Did it matter that this took place without membership approval? Well, The legal firm Walker Morris says these are the proper steps - in order:

|

QUESTION: So why did the

blunder-prone BSS Council - who

spent the equivalent of approximately 117 annual memberships

on TWO sets of legal advice on this, not do things in the right order?

As if all this was not enough (1) BSS's very own Independent Examiner (IEL Ltd) said: "If you're planning to set up a CIO or convert to one, there's one area which seems to be throwing up difficulties. Teething issues seem to be getting resolved but the question of the bank account can be a thorny issue. Stories are coming through of charities taking months, anything up to a year even, to open a bank account". Has this been sorted yet by BSS? Interestingly the increasingly secretive Council has never said. CIO's can be set up in 40 days and you might think that spending a fortune on two London law firms would have ensured that. As of August 2014 it was six months since the CIO was registered and STILL there was no progress. Members wanted to know the truth and whether this was another case of 'Blundering BSS'? Members heard nothing on the matter in the then recent June Newsletter - Why?

As if all this was not enough (2) it

turned out that BSS had only recently realised that they do not own the BSS

Trademark Logo. Can you really believe it?

[Point of Information: They still do not own it in 2016]!

|

NB: Only BSS Members in good standing could cast their vote at an AGM.

|

This page provided Guidance to those BSS

Members

All information was (and still is) provided here in good faith and only in summary form for the

information of visitors to this page. See our disclaimer at the bottom.

1. The Charitable Incorporated Organisation (CIO) was a

relatively new form of charity which

had only been available since January 1st 2013 and then not applicable to

charities of the size of BSS until mid 2013.

2. The Trustees of a Charitable Trust, such as BSS was before, remain subject to

general charity law and must always act with appropriate care and must keep

within the charitable objects and powers. Trustees/Directors of a charitable company

on the other hand

are additionally subject to the Companies Acts and various company law

requirements.

3. The chief attraction of registering as a CIO is that it provides protection

for the individual Trustees/Directors from personal financial liability in some

circumstances where Trustees of an unincorporated charitable trust would not be

protected. Another benefit of the CIO is that it provides the protection of limited

liability without the need to register with Companies House and the subsequent

reporting and company law requirements.

4. The main trigger for becoming a CIO is to give the charity the benefit of

limited liability through the CIO structure. The charity would benefit from

being a separate legal entity where its assets are at stake and not those of the

Trustees/Directors individually should it become bankrupt. The

Trustees/Directors of a

charitable company are responsible for ensuring that the charity meets with the

requirements of both Companies House and the Charity Commission at

all times. The CIO is designed for small to medium charities where contracts are

entered into and where staff might be employed.

5. There are two sets of potential liabilities that Trustees of a

Charitable Trust like BSS currently face. The first is in respect of the duties owed to the charity to act with the

necessary care and not to act outside the objects and powers of the charity. If

Trustees cause a loss to the charity, either through a lack of proper care or by

spending money for purposes outside the charity’s objects, they can be called

upon to refund the money out of their own resources. This applies as much to

Directors of a CIO as it does to the Trustees of an unincorporated charity.

The second has to do with potential claims by third parties. Examples of these

would be: claims for damages for personal injuries; claims for compensation for

unfair dismissal by an employee; claims for breach of contract by a supplier of

goods and services; claims for damages in respect of “wrong” counselling or other advice.

It is in respect of these potential claims that protection is afforded to the

Trustees/Directors of a CIO.

6. In the case of a CIO, a separate legal entity exists. This means that any

debts owed by the company are owed by the CIO and not by the Trustees/Directors

personally; assuming always that the Trustees have not given personal guarantees

or entered into contracts in a personal capacity. In the case of a Charitable

Trust such as that currently governing BSS, there is no separate corporate

entity, and therefore the debts and potential liabilities of the Charity, which

cannot be met out of its own resources, can become the liability of the Trustees

personally.

7. It should be added that in the case of a CIO, if the Trustees/Directors continue

to operate whilst knowing that the company is insolvent, they could then become

personally liable for debts owed by the company.

8. A CIO exists as a separate legal entity, legal title to buildings, stocks and

shares etc., can be held in the name of the CIO and not in the names of the

Trustees/Directors for the time being. This saves legal costs and fees associated with a

change of legal title of land/buildings when Trustees/Directors change. But it should be

noted that it is entirely possible to incorporate a body of Trustees of a

Charitable Trust so that legal title can be held in a corporate name. This is

called a Trust Corporation. However, this does not give the Trustees the

protection of limited liability.

9. The present Charitable Trust structure of BSS had the benefit of simplicity.

Trust Deeds usually leave the Trustees to decide how often they meet and how

they convene their meetings etc. They ought to keep minutes of their meetings,

although this is not a formal legal requirement.

CIOs on the other hand face stricter requirements under the Companies Acts.

Unless the charitable company’s Articles of Association provides the provision

to dispense with holding an AGM, one will have to be held at the right time each

year with proper notice given of the time and place and the business to be

transacted. At the moment unless the BSS Trustees decide otherwise the AGM is

there solely to elect the persons who will serve as Trustees for the next year. Annual returns and notices of changes of

Trustees/Directors or Secretary or

the Registered Office have to be notified to Companies House within certain time

limits. Accounts must be sent to Companies House within strict time limits. Late

filing of the annual accounts brings an immediate fine of £150, which increases

if the delay is more than one month. There are also specific requirements regarding

details that must be present on all Company notepaper.

10. CIOs must maintain a Register of Trustees which is open to anyone to view,

and a Register of Members which is not open to anyone to view. In the case of a

Charitable Trust, an annual return and accounts

must be submitted to the Charity Commission each year. An AGM must also be held every

year. The Charities Act 2011 does not allow Trustees of a charitable trust

(like BSS is at the moment) to dispense with these, as is the case with a

charitable company).

11. The requirements are broadly similar for charitable trusts and CIOs in that

the Charities Accounting Regulations have placed equal expectations to keep

accounting records and to produce annual accounts to certain standards on both

unincorporated charities and CIOs. It is understood that full accrual accounting

will generally be required after conversion to a CIO. This will undoubtedly limit the number of

members who could be readily persuaded to offer themselves as Treasurer.

12. For charities and for CIOs with turnover and fixed assets under £500,000,

an Independent Examination is required; as now.

13. A significant cost is involved in setting up a CIO, the more so if external

assistance is being used for this as was the case with BSS.

14. The Charity Commission now takes the view that a CIO is a successor body to

the original Charitable Trust. If a gift is made to a dissolved unincorporated

charity it would take effect as a gift for the purposes of the association. A

statement showing that the new body is succeeding the original charity and that

the charitable objects are the same may be included within the Memorandum and

Articles, or the Constitution (in the case of a CIO). In addition, an

incorporating charity can be listed on the Charity Commission’s Register of

Mergers as a charity having transferred its assets to another (i.e. the new

incorporated charity).

15. Following incorporation, all contracts and assets had to be transferred to

the new entity. Liabilities may not normally be transferred into the new

organisation.

16. Read comments here in the media about the introduction of CIOs. ►Media interest in CIOs (Guardian) ►Media Interest in CIOs (Charity Times)

17. Other information ►Here from Deloittes

[Back]

This summary is provided in good faith as a short outline

intended as information for members of BSS and other interested parties.

It only covers CIOs and their differences with established Charitable Trusts.

It is not an exhaustive summary of the legal status of CIOs and it certainly

does not represent legal opinion.

Advice should be sought before reliance is

placed on the content of this page. Information published with permission

E.&O.E.

Please advise the webmaster if

anything here is incorrect or needs better explanation.

09/04/2016